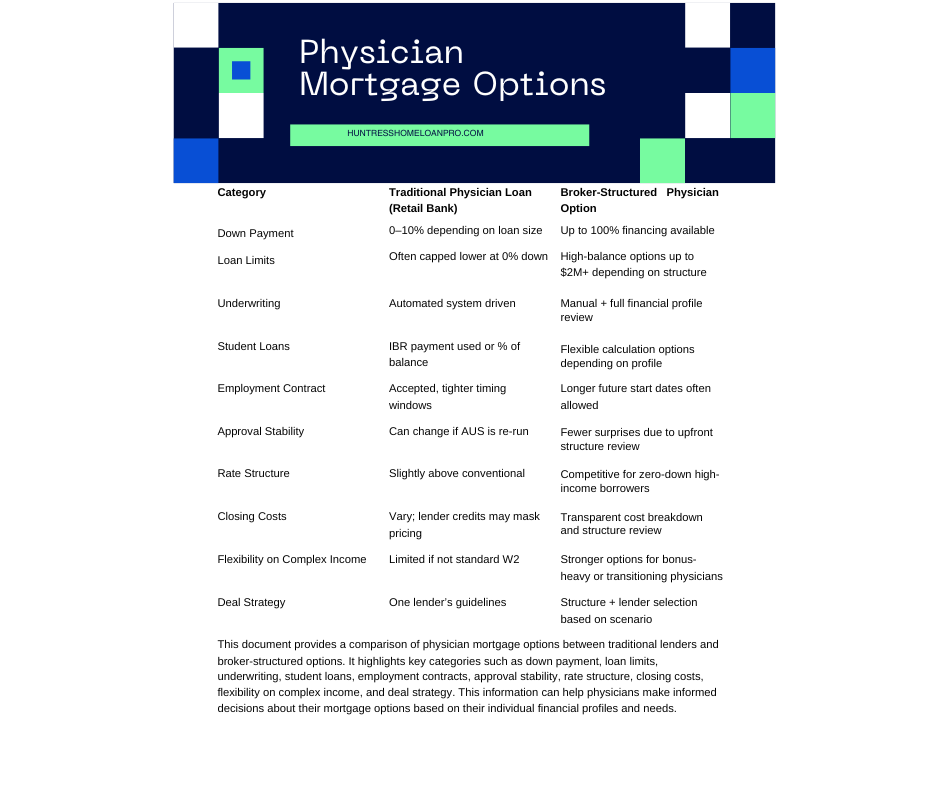

Not All Physician and Medical Provider Loans Are Built The Same

What Doctors (And Their Agents) Should Know...

If you’re a physician, resident, fellow, dentist, pharmacist, CRNA, or veterinarian, you may have heard:

“You can buy with zero down and no mortgage insurance.”

That’s true.

What’s not talked about enough is this:

Not all physician loans are structured the same.

And at $1.5M–$2M purchase prices, structure matters more than headline marketing.

As a mortgage broker, I don’t have one physician loan.

We now have multiple physician-specific structures — and they are built very differently.

Let’s break that down.

The Myth: “A Doctor Loan Is a Doctor Loan”

Retail banks often offer:

- One physician product

- Automated underwriting

- Internal overlays

- Limited flexibility

- Strict DTI caps

- Tight projected income windows

That works — until it doesn’t.

Where deals start to wobble:

- Large student loan balances

- Start dates 4–5 months out

- High DTI due to zero-down jumbo pricing

- Contract bonuses or sign-on income

- Rapid career transitions

This is where structure becomes critical.

What Makes Broker Physician Structures Different?

As a broker, I can access:

✔ Manual Underwritten Physician Programs

A human underwriter reviews the full file — not just an algorithm.

That means:

- Compensating factors matter

- Asset strength matters

- Professional trajectory matters

- Context matters

On $1.8M purchases, that difference can save a deal.

✔ Higher Loan Limits at 100% Financing

Some of our physician programs allow:

- Up to $1.5M–$2M with zero down (credit dependent)

- No mortgage insurance

- Competitive DTI tolerances

Retail programs often taper down payment requirements as loan size increases.

✔ Student Loan Treatment That Makes or Breaks Approval

Depending on structure:

- Residency income can be used strategically

- Student loans may be excluded in specific residency scenarios

- Or calculated differently than conventional guidelines

On a $400,000 student loan balance, this can change qualifying power dramatically.

✔ Projected Income Flexibility

Some of our medical programs allow:

- Fully executed contracts

- Start dates up to 150 days out

- Standard employment contingencies only

Many retail banks tighten this window.

✔ Jumbo ARM Options That Are Assumable

Some physician ARMs:

- Are assumable

- Offer 5/6, 7/6, 10/6 structures

- Provide rate strategy flexibility

- Work well for short-term relocation or hospital track movement

Strategic, not emotional decisions.

Let’s Talk About Rates & Costs

Zero-down physician loans are specialty jumbo products.

That means:

- Rates are typically slightly higher than 20% down conventional loans

- Pricing reflects increased lender risk

- Closing costs vary based on structure and lender

What matters most isn’t the headline rate.

It’s:

- Total cost

- Stability of approval

- Underwriting confidence

- Whether the deal survives appraisal and final review

At $1.8M, volatility is expensive.

When Structure Matters Most

Broker physician programs shine when:

- High student loan debt

- 45–50% DTI scenarios

- Large zero-down jumbo loans

- Start date income scenarios

- Complex compensation structures

- Borrowers who need a manual review

A retail product may work beautifully for a clean $800K deal.

It may not hold at $1.8M.

The Real Advantage

I don’t sell “a doctor loan.”

I evaluate:

- Debt structure

- Contract timing

- Asset positioning

- Rate strategy

- Long-term mobility

- Risk of late-stage denial

And then I help you select the right structure.

That’s the difference between shopping and structuring.

You deserve guidance.

You deserve options.

And yes—you deserve a home, you've earned it. 💪🏡

Theresa Rolen – The Huntress Home Loan Pro

Mortgage Loan Originator

Phone:913-705-0049

Email:Theresa@SummitLendingUSA.com

NMLS #2249004 | Summit Lending NMLS #1850081 | Equal Housing Opportunity |https://nmlsconsumeraccess.org/

Book a 1:1 Strategy Call:

https://calendly.com/theresa-summitlending